At the economic debates held in the Parliament of Georgia on 1 October 2013, Member of the Parliamentary Majority Paata Kvizhinadze stated in his speech: “As of today, the Council of Appeals at the Ministry of Finance went from formal activities to real actions. It examines problematic matters and in most cases makes a decision in favour of entrepreneurs.”

FactCheck inquired about the accuracy of facts indicated in the MP’s statement and set out to check what had changed in the work of the Council of Tax Appeals of the Ministry of Finance. For this reason we looked into the dynamics of decisions made on the cases in recent years.

The Council of Tax Appeals is a tax dispute resolution body under the Ministry of Finance of Georgia. The Council is headed by the Minister of Finance and its members represent different governmental bodies as well as non-governmental organisations.

The tax dispute resolution system within the Ministry of Finance consists of two stages and starts with the submission of an appeal at the Revenue Service. In the case of an undesirable decision, a taxpayer has the right to lodge an appeal at the Council of Tax Appeals. The taxpayer is empowered to apply to the Court at any stage of the dispute at the Ministry of Finance.

Certain changes have been introduced into the work of the Council since the end of 2012; particularly:

As reported by the Council, since December of 2012 the Council of Tax Appeals recognises the precedential nature of its decisions which is manifested in the Council’s obligation to make similar decisions on analogous cases. The Council maintains a special right, however, to divert from its established practice (Golden Rule) and introduce new a proceeding provided while making the new decision it finds that the established practice requires revision and supports its view with solid arguments.

In line with the established practice, deciding upon a specific case, the Council points out a certain previous decision as an analogy which provides a base for the solution of the case. In the case if after a specific decision has been made by the Council it becomes evident that the case bears significant, previously unnoticed, unexplained differences with the established practice, the Council is then compelled to make relevant clarification.

Decisions of the Council of Tax Appeals are published on the website of the Council without the identification information of the subject of the dispute.

With the initiative of the Ministry of Finance representatives of the non-governmental organisation sector are given the right to take part in the work of the Council of Tax Appeals. In order to ensure participation of a wide spectrum of non-governmental organisations the members of the Council are rotated every six months. A representative of the tax Ombudsman participates in the work of the Council as well.

In order to establish how the changes introduced into the work of the Council affected its decisions, that is to say whether or not the Council had moved “from formal activities to real actions,” FactCheck compared the data depicting the Council’s work of the current year to the statistics of previous years.

In line with the information provided by the Ministry of Finance, throughout the first three quarters of 2013, of 1,416 appeals, the Council of Tax Appeals conducted proceedings on 765 cases. The Council has partially or fully satisfied 54% (411 cases) of the complaints, 27% of the lodged appeals were not satisfied and 19% (145 cases) have not been examined. As gathered from the data of three quarters of 2013, the disputed amount totalled GEL 202.5 million.

The data of the first three quarters of the current year shows that this year’s percentage of partially or fully satisfied complaints already exceeds the same indicator of the previous year. At this point in time, the difference equals 7%. The said indices of 2013 also surpass the percentage of partially or fully satisfied appeals of 2009 and 2010 but fall behind the indicator present in 2011 by 13%.

The data of the first three quarters of the current year shows that this year’s percentage of partially or fully satisfied complaints already exceeds the same indicator of the previous year. At this point in time, the difference equals 7%. The said indices of 2013 also surpass the percentage of partially or fully satisfied appeals of 2009 and 2010 but fall behind the indicator present in 2011 by 13%.

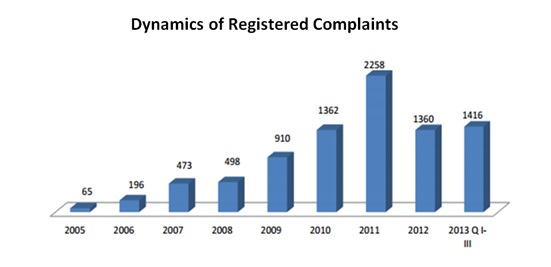

In line with the data of three quarters of 2013, the number of complaints registered in the Council of Tax Appeals already surpasses the same indicator from the last year. Currently, the difference amounts to 56 complaints. The data of the first three quarters of the current year also exceeds the number of appeals registered at the Council in each year from 2005 to 2010 but, at this point, falls behind the indices of 2011 by 843 appeals. In the period between 2005 and 2011 the number of registered appeals was characterised with an uninterrupted tendency of an increase.

In line with the data of three quarters of 2013, the number of complaints registered in the Council of Tax Appeals already surpasses the same indicator from the last year. Currently, the difference amounts to 56 complaints. The data of the first three quarters of the current year also exceeds the number of appeals registered at the Council in each year from 2005 to 2010 but, at this point, falls behind the indices of 2011 by 843 appeals. In the period between 2005 and 2011 the number of registered appeals was characterised with an uninterrupted tendency of an increase.

Notwithstanding the fact that in the first three quarters of 2013 the number of appeals already exceeded the same indicators of previous years, the figure for the disputed amount is lower than in 2012 by GEL 90.5 million. The disputed amount registered in the current year surpasses only those registered in 2006-2008. Over the years 2010-2012 the figures of the disputed amount see a decrease.

Conclusion

Staring from 2012, certain changes have been introduced into the work of the Council of Tax Appeals at the Ministry of Finance. With the initiative of the Ministry, the non-governmental sector was granted the right to take part in the work of the Council. In order to ensure participation of a broad spectrum of non-governmental organisations, the members of the Council are rotated every six months. The Council recognised the precedential nature of its decisions. In pursuance of further increasing transparency of the Council’s work and reinforcing the establishment of a coherent practice, the decisions of the Council of Tax Appeals are published on the website of the Council. Analysing the data on decisions made by the Council of Tax Appeals in the first three quarters of 2013 against the statistics of recent years, we see that the disputed amount continues a tendency of decrease so far but the number of registered complaints exceeds the same indicator of previous years. As gathered from the data of the first three quarters of 2013, the percentage of satisfied complaints (54%) surpasses the share of decisions satisfied in 2012 (47%). It is to be noted, however, that in 2010 and 2011 for instance, the sums disputed in the Council notably surpassed those of 2013 and the number of registered complaints was significantly higher in 2011 than so far in 2013. Furthermore, in 2011 the percentage of satisfied complaints amounted to 67% which exceeds the indicator of the first three quarters of 2013 by 13%.

Views may differ regarding the reasons underlying the change observed in the number of lodged complaints and in the size of the disputed amount (for example, amendments introduced into the legislation, political will and so forth)but it is not FactCheck’s intention to discuss those in this article. It is worthwhile noting, however, that the share of decisions made in favour of a plaintiff, for instance, was fairly high in 2011. This clearly denotes much more than “formal activities” of the Council as claimed by the MP.

Since the end of 2012, certain positive advances have been made in the work of the Council of Tax Appeals with regard to the participation of the non-governmental sector, the precedential nature and transparency of decisions. The comparison of the Ministry’s achievements of the first three quarters of 2013 with those of previous years, however, reveals that a high percentage of decisions made in favour of a plaintiff was witnessed, for instance, in 2011 as well. Therefore, we conclude that Paata Kvizhinadze’s statement, “As of today, the Council of Appeals at the Ministry of Finance went from formal activities to real actions. It examines problematic matters and in most cases makes a decision in favour of entrepreneurs,” is HALF TRUE.

Notwithstanding the fact that in the first three quarters of 2013 the number of appeals already exceeded the same indicators of previous years, the figure for the disputed amount is lower than in 2012 by GEL 90.5 million. The disputed amount registered in the current year surpasses only those registered in 2006-2008. Over the years 2010-2012 the figures of the disputed amount see a decrease.

Conclusion

Staring from 2012, certain changes have been introduced into the work of the Council of Tax Appeals at the Ministry of Finance. With the initiative of the Ministry, the non-governmental sector was granted the right to take part in the work of the Council. In order to ensure participation of a broad spectrum of non-governmental organisations, the members of the Council are rotated every six months. The Council recognised the precedential nature of its decisions. In pursuance of further increasing transparency of the Council’s work and reinforcing the establishment of a coherent practice, the decisions of the Council of Tax Appeals are published on the website of the Council. Analysing the data on decisions made by the Council of Tax Appeals in the first three quarters of 2013 against the statistics of recent years, we see that the disputed amount continues a tendency of decrease so far but the number of registered complaints exceeds the same indicator of previous years. As gathered from the data of the first three quarters of 2013, the percentage of satisfied complaints (54%) surpasses the share of decisions satisfied in 2012 (47%). It is to be noted, however, that in 2010 and 2011 for instance, the sums disputed in the Council notably surpassed those of 2013 and the number of registered complaints was significantly higher in 2011 than so far in 2013. Furthermore, in 2011 the percentage of satisfied complaints amounted to 67% which exceeds the indicator of the first three quarters of 2013 by 13%.

Views may differ regarding the reasons underlying the change observed in the number of lodged complaints and in the size of the disputed amount (for example, amendments introduced into the legislation, political will and so forth)but it is not FactCheck’s intention to discuss those in this article. It is worthwhile noting, however, that the share of decisions made in favour of a plaintiff, for instance, was fairly high in 2011. This clearly denotes much more than “formal activities” of the Council as claimed by the MP.

Since the end of 2012, certain positive advances have been made in the work of the Council of Tax Appeals with regard to the participation of the non-governmental sector, the precedential nature and transparency of decisions. The comparison of the Ministry’s achievements of the first three quarters of 2013 with those of previous years, however, reveals that a high percentage of decisions made in favour of a plaintiff was witnessed, for instance, in 2011 as well. Therefore, we conclude that Paata Kvizhinadze’s statement, “As of today, the Council of Appeals at the Ministry of Finance went from formal activities to real actions. It examines problematic matters and in most cases makes a decision in favour of entrepreneurs,” is HALF TRUE.

The data of the first three quarters of the current year shows that this year’s percentage of partially or fully satisfied complaints already exceeds the same indicator of the previous year. At this point in time, the difference equals 7%. The said indices of 2013 also surpass the percentage of partially or fully satisfied appeals of 2009 and 2010 but fall behind the indicator present in 2011 by 13%.

In line with the data of three quarters of 2013, the number of complaints registered in the Council of Tax Appeals already surpasses the same indicator from the last year. Currently, the difference amounts to 56 complaints. The data of the first three quarters of the current year also exceeds the number of appeals registered at the Council in each year from 2005 to 2010 but, at this point, falls behind the indices of 2011 by 843 appeals. In the period between 2005 and 2011 the number of registered appeals was characterised with an uninterrupted tendency of an increase.

Notwithstanding the fact that in the first three quarters of 2013 the number of appeals already exceeded the same indicators of previous years, the figure for the disputed amount is lower than in 2012 by GEL 90.5 million. The disputed amount registered in the current year surpasses only those registered in 2006-2008. Over the years 2010-2012 the figures of the disputed amount see a decrease.

Conclusion

Staring from 2012, certain changes have been introduced into the work of the Council of Tax Appeals at the Ministry of Finance. With the initiative of the Ministry, the non-governmental sector was granted the right to take part in the work of the Council. In order to ensure participation of a broad spectrum of non-governmental organisations, the members of the Council are rotated every six months. The Council recognised the precedential nature of its decisions. In pursuance of further increasing transparency of the Council’s work and reinforcing the establishment of a coherent practice, the decisions of the Council of Tax Appeals are published on the website of the Council. Analysing the data on decisions made by the Council of Tax Appeals in the first three quarters of 2013 against the statistics of recent years, we see that the disputed amount continues a tendency of decrease so far but the number of registered complaints exceeds the same indicator of previous years. As gathered from the data of the first three quarters of 2013, the percentage of satisfied complaints (54%) surpasses the share of decisions satisfied in 2012 (47%). It is to be noted, however, that in 2010 and 2011 for instance, the sums disputed in the Council notably surpassed those of 2013 and the number of registered complaints was significantly higher in 2011 than so far in 2013. Furthermore, in 2011 the percentage of satisfied complaints amounted to 67% which exceeds the indicator of the first three quarters of 2013 by 13%.

Views may differ regarding the reasons underlying the change observed in the number of lodged complaints and in the size of the disputed amount (for example, amendments introduced into the legislation, political will and so forth)but it is not FactCheck’s intention to discuss those in this article. It is worthwhile noting, however, that the share of decisions made in favour of a plaintiff, for instance, was fairly high in 2011. This clearly denotes much more than “formal activities” of the Council as claimed by the MP.

Since the end of 2012, certain positive advances have been made in the work of the Council of Tax Appeals with regard to the participation of the non-governmental sector, the precedential nature and transparency of decisions. The comparison of the Ministry’s achievements of the first three quarters of 2013 with those of previous years, however, reveals that a high percentage of decisions made in favour of a plaintiff was witnessed, for instance, in 2011 as well. Therefore, we conclude that Paata Kvizhinadze’s statement, “As of today, the Council of Appeals at the Ministry of Finance went from formal activities to real actions. It examines problematic matters and in most cases makes a decision in favour of entrepreneurs,” is HALF TRUE.