At the session of the Parliament, the Chairperson of the Georgian Dream Parliamentary Faction, Giorgi Volski, emphasised the role of the National Bank of Georgia in the process of the depreciation of GEL. Mr Volski asserted: "The recommendation of the International Monetary Fund was to issue consumer loans in GEL only. However this recommendation was not taken into account. Moreover, it was not even discussed."

FactCheck verified the accuracy of the statement.

In countries which do not have a fixed exchange rate, a loan issued in a foreign currency without a natural or financial hedging (reduction of risks to insure oneself against the losses which might occur if the circumstances under which the contract was signed suddenly change unfavourably) bears a significant risk. An example of natural hedging is an exporter who has income in USD. Therefore, even if his loan is denominated in USD, he is naturally safeguarded from the currency associated risks (his income and expenses are both in the same currency).

The high share of foreign currency denominated loans which are issued for non-hedged borrowers might be risky not only for certain borrowers but entails a danger for the whole financial sector as well. Normally, the business sector has greater capabilities to predict the risks and minimise them independently but in order to reduce financial risks, it is generally encouraged to issue national currency denominated loans for the more vulnerable borrowers – family farms. This approach is aimed at increasing financial stability and international organisations of the respective profile urge local policy-making organisations to pay close attention to this topic. In its analysis of the stability of the financial sector, the International Monetary Fund (IMF) also recommended the National Bank of Georgia use every instrument at its disposal to encourage the issue of national currency denominated loans.

The need to encourage the "larisation" (increase of the share of GEL) in the financial sector has been constantly underlined in the annual reports published by the National Bank of Georgia. The National Bank considered the low level of "larisation" as risky and in order to improve the situation tried to use the financial market to influence the behaviour of economic agents. According to the 2012 report (p. 10) of the National Bank, in this regard the most active measures were taken in 2009. These measures included the activation of monetary instruments, the introduction of a currency auction and the expansion of the mortgage market together with other appropriate steps. The International Monetary Fund also emphasises the measures taken by the National Bank of Georgia. The programme, published by the IMF, directly points out that the National Bank of Georgia had used a set of measures to make the issue of foreign currency denominated loans more expensive for commercial banks. This policy is unequivocally regarded as a step toward "larisation" because commercial banks have reduced the incentive to issue foreign currency denominated loans. The rise of the weighted risk of a foreign currency denominated loan to 175% is given by the IMF as an example. The result of the policy of the National Bank of Georgia, aimed to increase "larisation," is depicted in Graph 1.

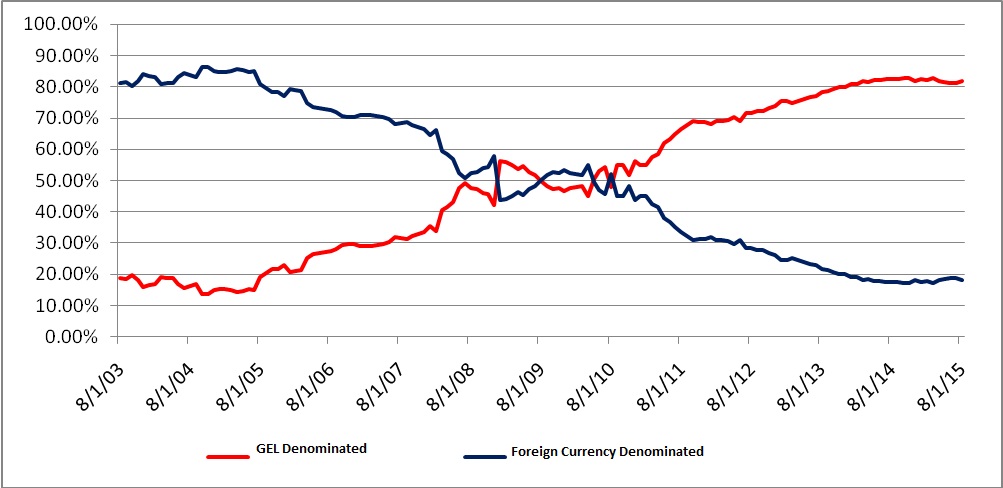

Graph 1: Entire Structure of Consumer Loans Issued in 2003-2015

Source: National Bank of Georgia

As illustrated in the graph, the share of GEL denominated consumer loans has been on a permanent rise in the total amount of loans since 2003. The only exception is the post-crisis years of 2008-2010 when a relative fluctuation did take place. As of 1 August 2015, the share of GEL denominated consumer loans stood at 81.8% and was only 1.02% less than the absolute maximum of 82.8% which was registered in November 2014. Graph 2 shows the structure of loans issued entirely for family farm households.

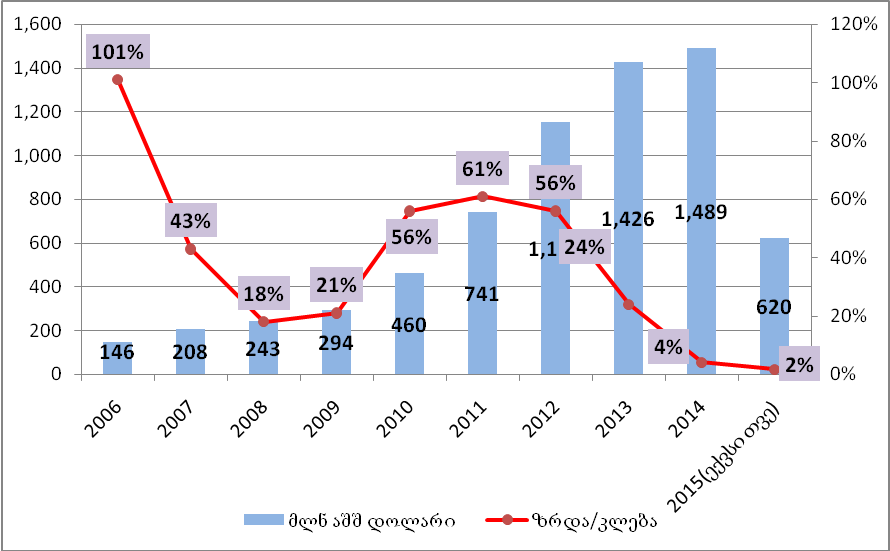

Graph 2: Loans for Households Issued in 2003-2015

Source: National Bank of Georgia

As illustrated in the graph, the share of GEL denominated consumer loans has been on a permanent rise in the total amount of loans since 2003. The only exception is the post-crisis years of 2008-2010 when a relative fluctuation did take place. As of 1 August 2015, the share of GEL denominated consumer loans stood at 81.8% and was only 1.02% less than the absolute maximum of 82.8% which was registered in November 2014. Graph 2 shows the structure of loans issued entirely for family farm households.

Graph 2: Loans for Households Issued in 2003-2015

Source: National Bank of Georgia

As illustrated in the graph, the "larisation" policy has certain difficulties when it comes to the structure of loans issued for family farms. These indicators include mortgage loans as well which due to their duration and volume might become a heavy burden for each borrower under a currency fluctuation.

Conclusion

The high share of foreign currency denominated loans issued for borrowers who are less protected from the risks is dangerous both for the financial sectors and for certain borrowers whose income is in GEL whilst their loan is in USD. Therefore, the International Monetary Fund has always recommended the National Bank of Georgia encourage the issuing of national currency denominated loans. Thus, the MP is correct to underline the existence of such a recommendation.

The annual publications of the National Bank of Georgia have been constantly emphasising the risks caused by the low share of GEL denominated loans. According to its 2012 report, the development of the bond market resulted in the increased liquidity of the financial markets and the stabilisation of interest rates. These enabled commercial banks to use GEL actives more vigorously. The certain measures taken by the National Bank of Georgia are positively evaluated by the International Monetary Fund in the financial sector evaluation programme published in 2015. The structural dynamic of consumer loans proves the effectiveness of the measures taken to increase the "larisation" of consumer loans.

At the same time, it is necessary to underscore that the structure of consumer loans issued for family farms is less positive.

FactCheck concludes that Giorgi Volski’s statement is FALSE.

Source: National Bank of Georgia

As illustrated in the graph, the "larisation" policy has certain difficulties when it comes to the structure of loans issued for family farms. These indicators include mortgage loans as well which due to their duration and volume might become a heavy burden for each borrower under a currency fluctuation.

Conclusion

The high share of foreign currency denominated loans issued for borrowers who are less protected from the risks is dangerous both for the financial sectors and for certain borrowers whose income is in GEL whilst their loan is in USD. Therefore, the International Monetary Fund has always recommended the National Bank of Georgia encourage the issuing of national currency denominated loans. Thus, the MP is correct to underline the existence of such a recommendation.

The annual publications of the National Bank of Georgia have been constantly emphasising the risks caused by the low share of GEL denominated loans. According to its 2012 report, the development of the bond market resulted in the increased liquidity of the financial markets and the stabilisation of interest rates. These enabled commercial banks to use GEL actives more vigorously. The certain measures taken by the National Bank of Georgia are positively evaluated by the International Monetary Fund in the financial sector evaluation programme published in 2015. The structural dynamic of consumer loans proves the effectiveness of the measures taken to increase the "larisation" of consumer loans.

At the same time, it is necessary to underscore that the structure of consumer loans issued for family farms is less positive.

FactCheck concludes that Giorgi Volski’s statement is FALSE.

Source: National Bank of Georgia

As illustrated in the graph, the share of GEL denominated consumer loans has been on a permanent rise in the total amount of loans since 2003. The only exception is the post-crisis years of 2008-2010 when a relative fluctuation did take place. As of 1 August 2015, the share of GEL denominated consumer loans stood at 81.8% and was only 1.02% less than the absolute maximum of 82.8% which was registered in November 2014. Graph 2 shows the structure of loans issued entirely for family farm households.

Graph 2: Loans for Households Issued in 2003-2015

Source: National Bank of Georgia

As illustrated in the graph, the "larisation" policy has certain difficulties when it comes to the structure of loans issued for family farms. These indicators include mortgage loans as well which due to their duration and volume might become a heavy burden for each borrower under a currency fluctuation.

Conclusion

The high share of foreign currency denominated loans issued for borrowers who are less protected from the risks is dangerous both for the financial sectors and for certain borrowers whose income is in GEL whilst their loan is in USD. Therefore, the International Monetary Fund has always recommended the National Bank of Georgia encourage the issuing of national currency denominated loans. Thus, the MP is correct to underline the existence of such a recommendation.

The annual publications of the National Bank of Georgia have been constantly emphasising the risks caused by the low share of GEL denominated loans. According to its 2012 report, the development of the bond market resulted in the increased liquidity of the financial markets and the stabilisation of interest rates. These enabled commercial banks to use GEL actives more vigorously. The certain measures taken by the National Bank of Georgia are positively evaluated by the International Monetary Fund in the financial sector evaluation programme published in 2015. The structural dynamic of consumer loans proves the effectiveness of the measures taken to increase the "larisation" of consumer loans.

At the same time, it is necessary to underscore that the structure of consumer loans issued for family farms is less positive.

FactCheck concludes that Giorgi Volski’s statement is FALSE.

Tags: