Irakli Kovzanadze: “Under high dollarisation and import-dependency, the deficit growth leads to higher macroeconomic risks. The loan attraction increased and currently we have a 60.1% debt to GDP ratio with a large portion of foreign loans. When most of the foreign debt is denominated in foreign currency, increased risks hamper the consolidation of budget revenues and appropriations.”

Verdict: FactCheck concludes that Irakli Kovzanadze’s statement is TRUE.

Analysis:

Chairperson of the Budget and Finance Committee of the Parliament of Georgia, Irakli Kovzanadze, stated: “Naturally, the deficit was poised to grow. We have high dollarisation and import-dependency. Under these conditions, the deficit growth leads to higher macroeconomic risks when the deficit grew, loan attraction also increased and currently we have a 60.1% debt to GDP ratio. Here, it is important to take a look at the debt composition where the portion of foreign loans is large. When most of the foreign debt is denominated in foreign currency, increased risks hamper the consolidation of budget revenues and appropriations.”

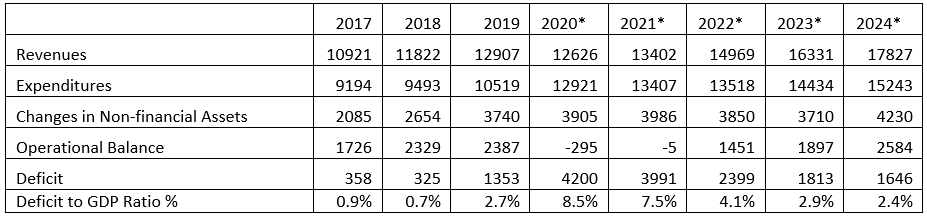

In the context of the COVID-19 pandemic, budget deficit growth is one of the critical problems. The difference between budget revenues and expenditures constitute a budget’s operational balance and the difference between the budget’s operational balance and the changes in non-financial assets (privatisation/selling property) is the total budget balance. The total positive balance is the budget surplus whilst the total negative balance is the budget deficit. The budget deficit means that the budget has less revenues as compared to expenditures and the government has to borrow to finance the difference. Apart from incurring expenses needed to fight the pandemic, deficit spending is also used to stimulate the pandemic-induced drop in consumption. However, this also entails a number of negative consequences such as inflation, downsized savings, higher interest rates, etc. In other words, the effect caused by the current deficit as well as the negative consequences associated with the growth of the foreign debt will be felt in the upcoming years. The threshold of the second macroeconomic parameter, as determined by Georgia’s Economic Liberty Act, is about the consolidated budget deficit. In particular, the consolidated budget’s deficit should not exceed 3% of the GDP. Therefore, the goal of this legislative commitment is to ensure that the government-planned expenditures do not substantially exceed the planned revenues. Budget planning or/and executing the planned parameters beyond the thresholds set by this law is possible under Georgian legislation in the case of a declaration of martial law or a state of emergency and if there is a need to fund measures to liquidate those consequences which arose as a result of the declaration of martial law/state of emergency. At the same time, the Government of Georgia has to submit a plan to the Parliament of Georgia to restore the legally prescribed parameters. The plan for returning back to the legally prescribed parameters should not exceed three years.

The forecasted figure for the consolidated budget deficit in 2020 is 8.5% which is 5.9 percentage points more and exceeds the legally allowed threshold. According to 2021’s plan, the consolidated budget deficit is 7.5%. Of note is that according to the preliminary data of the National Statistics Office of Georgia, the GDP decreased more than 5% as was the figure forecasted in the budget. Therefore, it is expected that the actual deficit for 2020, which is not yet available, is even larger as compared to the planned figure.

Table 1: Consolidated Budget Deficit in 2017-2014 (GEL Million, Forecasts)

Source: Ministry of Finance of Georgia

Georgia is an import-dependent country. Although export has been growing in the past years, import also grows annually. As a result, the trade deficit; that is, the difference between export and import, does not decrease substantially and fluctuates between USD 5.7 billion to USD 5.1 billion. In 2020 amid the pandemic, the foreign trade balance constituted USD 4.6 billion and this figure does not fit into the aforementioned trend. In spite of this, pressure on the exchange rate is naturally very high. GEL depreciation vis-à-vis foreign currencies directly impacts the government debt and deficit figures.

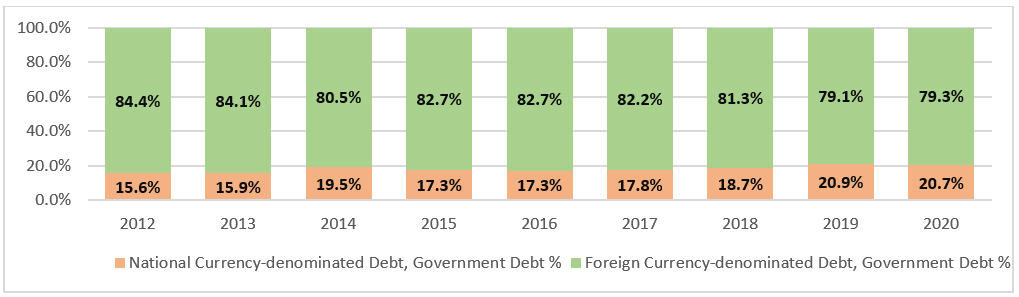

Government debt comprises domestic debt, denominated in a national currency, and foreign debt, denominated in a foreign currency. According to 2020’s data, the total government debt amounts to nearly GEL 29.5 billion which is approximately GEL 9.7 billion more as compared to the same period of the previous year and exceeds the legally allowed 60% threshold. Similar to the budget deficit, government debt over 60% is allowed for three years during the time of the pandemic. The GEL to USD exchange rate fluctuation is something take into account whilst analysing the government debt dynamic. In particular, both new debt (borrowed in one year) and the previously accumulated debt balance (the unpaid portion of a loan borrowed in the past) are recalculated amid the currency exchange rate fluctuation in accordance with a new exchange rate. In the last years, the growth of the government and the national debt was largely stipulated by a recalculation of the previously accumulated debt balance in accordance with the new exchange rate. The growth of the total government debt is mostly associated with the growth of the foreign debt. The domestic and foreign debt ratio as part of the total government debt is illustrated in Graph 2.

Graph 2: Ratio of Government Debt Figures Denominated in National and Foreign Currencies (GEL Shown at Graph) in 2012-2020

Source: Ministry of Finance of Georgia

In 2012-2020, the government debt’s foreign currency denominated portion was nearly 80% whilst the debt in the national currency was almost 20%. Naturally, servicing the increased debt stipulated by the budget deficit growth will become more expensive given GEL depreciation. In turn, this will give rise to some significant budget problems in the future. In particular, the government’s disposable funds will shrink and paying for the deficit will also be needed; therefore, the government will have to cut budget expenses and consolidate additional revenues which is a separate problem which will inevitably come true in the near future.