Koba Gvenetadze: "In the near past, Georgia has always been ahead of Armenia in terms of the credit rating”

Verdict: FactCheck concludes that Koba Gvenetadze’s statement is TRUE.

Resume:

Koba Gvenetadze’s statement was made in the context of the GEL depreciation dynamic vis-à-vis USD. In particular, GEL depreciated against USD by nearly 100% as compared to 2014 whilst this drop was by almost 25% as compared to 2020. At the same time, AMD depreciated vis-à-vis USD by 28% as compared to 2014 whilst the drop was by 10% as compared to 2020. The President of the National Bank of Georgia claimed that Georgia still had a better investment conjecture as compared to Armenia despite GEL losing its value vis-à-vis USD more than the loss experienced by AMD.

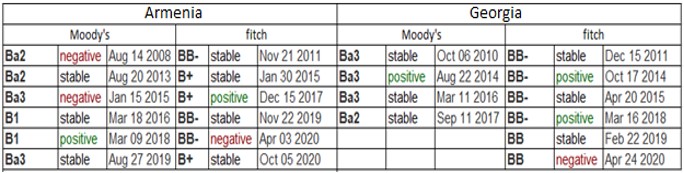

S&P did not assess Armenia’s rating and, therefore, only Fitch’s and Moody’s ratings presented in Table 2 can be used for comparison. In the context of currency depreciation starting from the third quarter of 2014, Georgia has indeed had a better investment position as compared to Armenia. However, of note is that Armenia had better rating than Georgia prior to January 2015 according to Moody’s. In case of Fitch, Armenia’s positions were especially weakened in 2015-2017. Naturally, problems sparking from the GEL exchange rate is part of the assessment criteria. Although, according to all relevant criteria, it is evident that Georgia is ahead of Armenia and the sharper depreciation of the Georgian currency vis-à-vis USD as compared to the AMD depreciation against USD had no impact on that. Both Georgia and Armenia are at a non-investment grade and there are speculative risks in their economies according to the assessment.

Analysis:

The President of the National Bank of Georgia, Koba Gvenetadze, on air on Rustavi 2 TV’s Ghamis Kurieri broadcast, stated: “Georgia has always been ahead of Armenia in terms of the credit rating.” This statement concerned the fluctuation of the GEL exchange rate. In particular, GEL depreciated against USD by nearly 100% as compared to 2014 whilst the drop was by almost 25% as compared to 2020. At the same time, AMD depreciated vis-à-vis USD by 28% as compared to 2014 whilst the drop was by 10% as compared to 2020. The argument of the President of the National Bank of Georgia was about Georgia having a better investment conjecture as compared to Armenia notwithstanding GEL losing more of its value as compared to AMD.

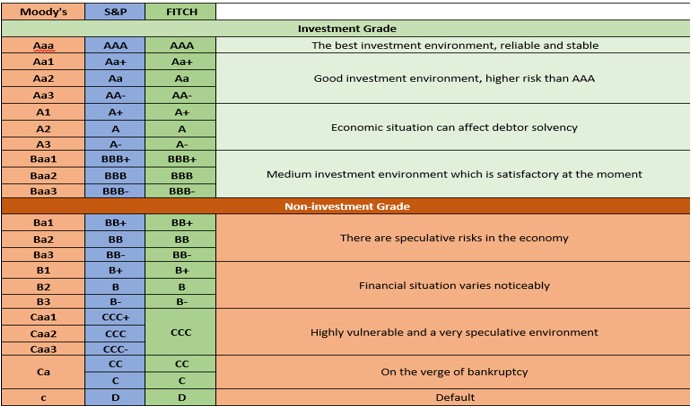

Countries compete in the world economy to attract foreign capital. Developing or less developed nations, which have their own limited resources, are particularly dependent upon foreign capital. In turn, creditors and investors make their choices by taking into account the rate of return and stability. In other words, they make calculations vis-à-vis possible profits and risks. The lower the risks (higher reliability), the lower the rate of return for the creditor or the investor of the capital in exchange for which he is ready to invest his money in the country. A country’s credit rating gives investors information about risk factors associated with investments in certain countries as well as the reliability of these countries. Dozens of agencies publish credit ratings although Standard & Poor’s (S&P), Moody’s and Fitch are the most influential and famous among them. Each credit rating agency employs its own methodology although basic indicators are the same and include economic indicators as well as a country’s domestic and foreign policies, regional processes and the environment.

Standard & Poor’s and Fitch employ similar assessment systems: AAA is the highest rating in their assessment which is followed by AA+, AA, AA- above average – A+, A, A-, below average – BBB+, BBB, BBB-, non-investment grade speculative – BB+, BB, BB-, speculative B+, B, B-, highly vulnerable CCC, on the verge of bankruptcy CC and default D. Moody’s assessment is also similar but instead of +/- it uses digitals: Aaa, Aa1, Aa2, Aa3, A1, A2, A3, Baa1, Baa2, Baa4, Ba1, Ba2, Ba3, B1, B2, B43, Caa1, Caa2, Caa3, Ca and C. Assessment levels in turn are divided into investment and non-investment grades. Table 1 shows the economic interpretation of these assessments. Furthermore, on top of their ratings, these companies give outlooks: negative, stable or positive. Table 1 shows the economic interpretation of these assessments.

Table 1: Assessments of Moody’s, S&P and Fitch and Interpretation of the Assessments

Source: www.bankersalmanac.com

S&P did not assess Armenia’s rating and, therefore, only Fitch’s and Moody’s ratings presented in Table 2 can be used for comparison. Roughly speaking, Georgia has indeed had a better investment position as compared to Armenia in the context of currency depreciation starting from the third quarter of 2014. However, of note is that Armenia had a better rating than Georgia prior to January 2015 according to Moody’s. In case of Fitch, Armenia’s positions were especially weakened in 2015-2017 and after 2020 Nagorno-Karabakh war. However, both Georgia and Armenia are at a non-investment grade and there are speculative risks in their economies according to the assessment.

Table 2: Georgia’s and Armenia’s ratings by Fitch and Moody’s

Source: tradingeconomics.com